Typologies of SME financing through private debt #2

What are the different types of private debt?

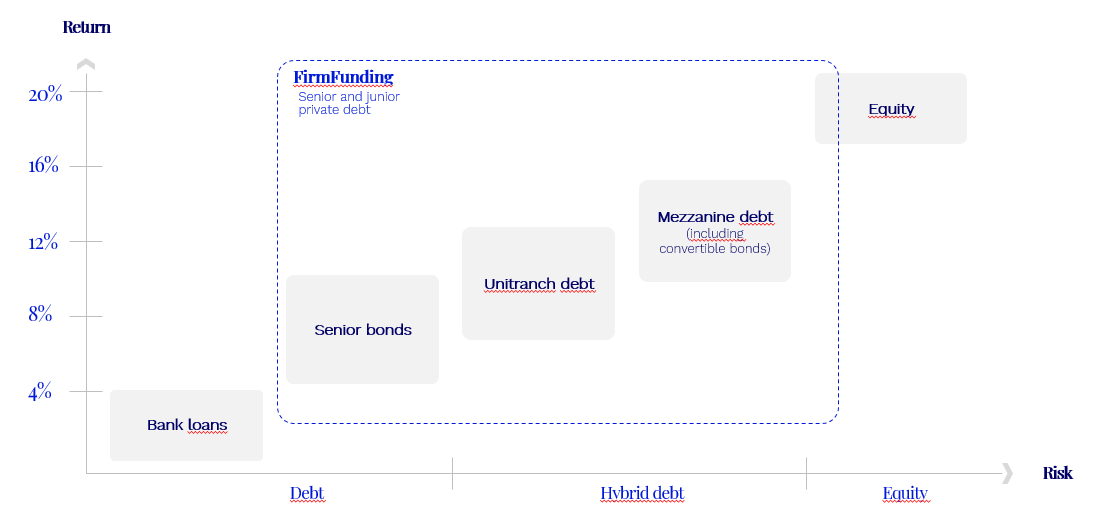

Over the past ten years, there has been a significant increase in the share of private debt in SMEs financing (see on this point the Banque de France study published in Bulletin No. 220/1 of September October 2018), allowing growth SMEs to finance genuine growth projects, by diversifying their sources of financing and the associated repayment terms (the bond holder allowing repayment in fine - see our previous study on eligibility conditions and the general characteristics of private debt here). But private debt covers several realities, depending on its performance, structure and repayment rank:

Senior debt, unitranche, mezzanine

Senior debt is the one with the highest priority at the time of repayment. It is a « pure » debt, without equity component. It is the least risky category and also the least expensive, often less than 10%. Its main advantage is that it is reimbursed in the end, giving the company time to carry out its development projects. It is therefore an essential intermediary for equity financing.

Mezzanine debt is always associated with other sources of financing between which it is inserted, as its name suggests. It is used as a complement to bank financing or senior debt on the one hand, and equity on the other, and will be integrated between these two tranches of financing. By nature, it is riskier than senior debt in the long term, since its repayment is subordinated to it, but it has priority over equity. The riskiest category of private debt because it is subordinated, its remuneration is often higher than 12%. His compensation generally has three components, including an equity component :

- periodic cash interest (quarterly, semi-annual or annual)

- an in fine interest capitalized

- an additional remuneration in the form of capital (BSA), which gives access to the capital gain realized, if any, on the investor's exit.

Mezzanine debt is particularly suitable for financing growth projects while optimising the development of SMEs, as it does not lead to immediate dilution and has a limited impact on cashflow. As part of an external growth operation, it increases the leverage and therefore the return to shareholders.

Unitranche debt, which combines, within a single tranche, a senior component and a mezzanine component, has the characteristics of mezzanine debt (periodic interest + capitalized in fine + Equity) but is not subordinated to the repayment of senior debt. As a result of this lower risk, its rate is also lower, ranging from 7 to 13%. Like mezzanine debt, unitranche debt is particularly suitable for SMEs in the development phase, which must mobilise their cashflow to finance their growth, particularly in the context of an acquisition. However, it has the advantage of placing the SME in front of a single interlocutor rather than a pool of creditors, which can save time and efficiency in setting up the operation.

Contact us

By email via the

contact form

By email via the

contact form